- Token Terminal

- Posts

- Why standardized reporting matters

Why standardized reporting matters

+ data & product updates

Each week in The Snapshot, we share data-driven insights, highlight new listings, and showcase our latest product updates.

Read on for the latest edition 👇

Traditional financial markets run on standardized reporting. Audited financials and quarterly earnings calls give investors the tools to evaluate individual businesses, benchmark them against each other, and allocate capital based on fundamentals.

Most projects with liquid tokens do not provide regular, standardized, and verified reporting to their stakeholders. In a market where investors have to make investment decisions with incomplete information, capital is at risk of going to the best narratives, instead of the best businesses.

Token Terminal's standardized reporting initiative exists to close this gap. Standardized metrics require ongoing maintenance as projects expand to new chains and launch new products, and Token Terminal updates the underlying datasets to keep pace.

What standardized reporting looks like

As part of its Data Partnership with Aave Labs, Token Terminal publishes monthly, data-driven reports on Aave’s onchain fundamentals. Each report includes granular breakdowns of different metrics; grouped by chain, product, asset, and more.

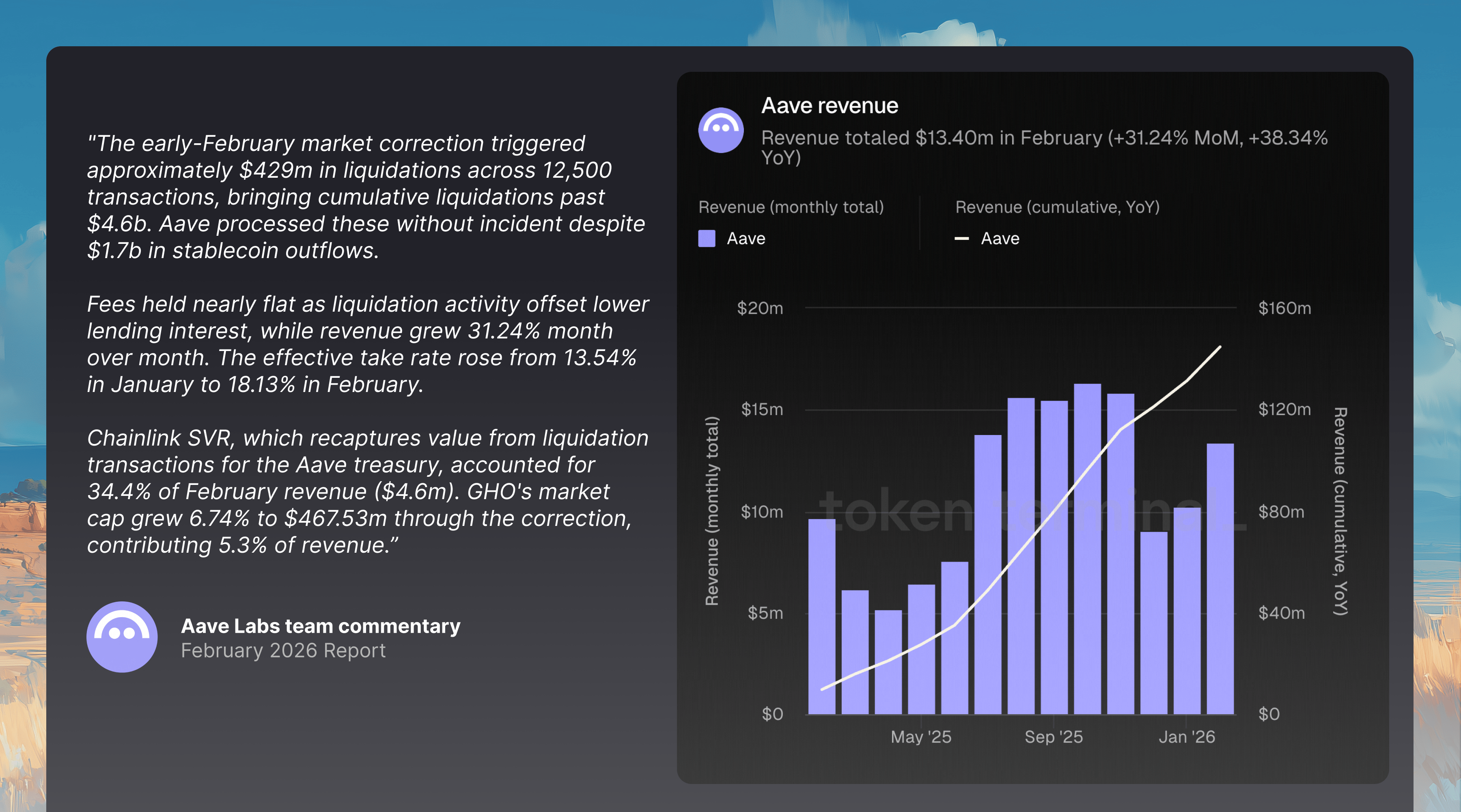

February's report landed during a sharp market downturn. TVL and active loans fell over 20%, while revenue grew over 30%. Aave's report makes this transparent to readers through standardized, quantitative data that shows exactly what happened and which metrics moved.

The report also includes direct commentary from the Aave Labs team. This gives the team a channel to contextualize the numbers on their own terms, explain operational decisions, and highlight developments that the data alone does not capture. For investors, it turns a dataset into a complete picture.

How Aave makes money

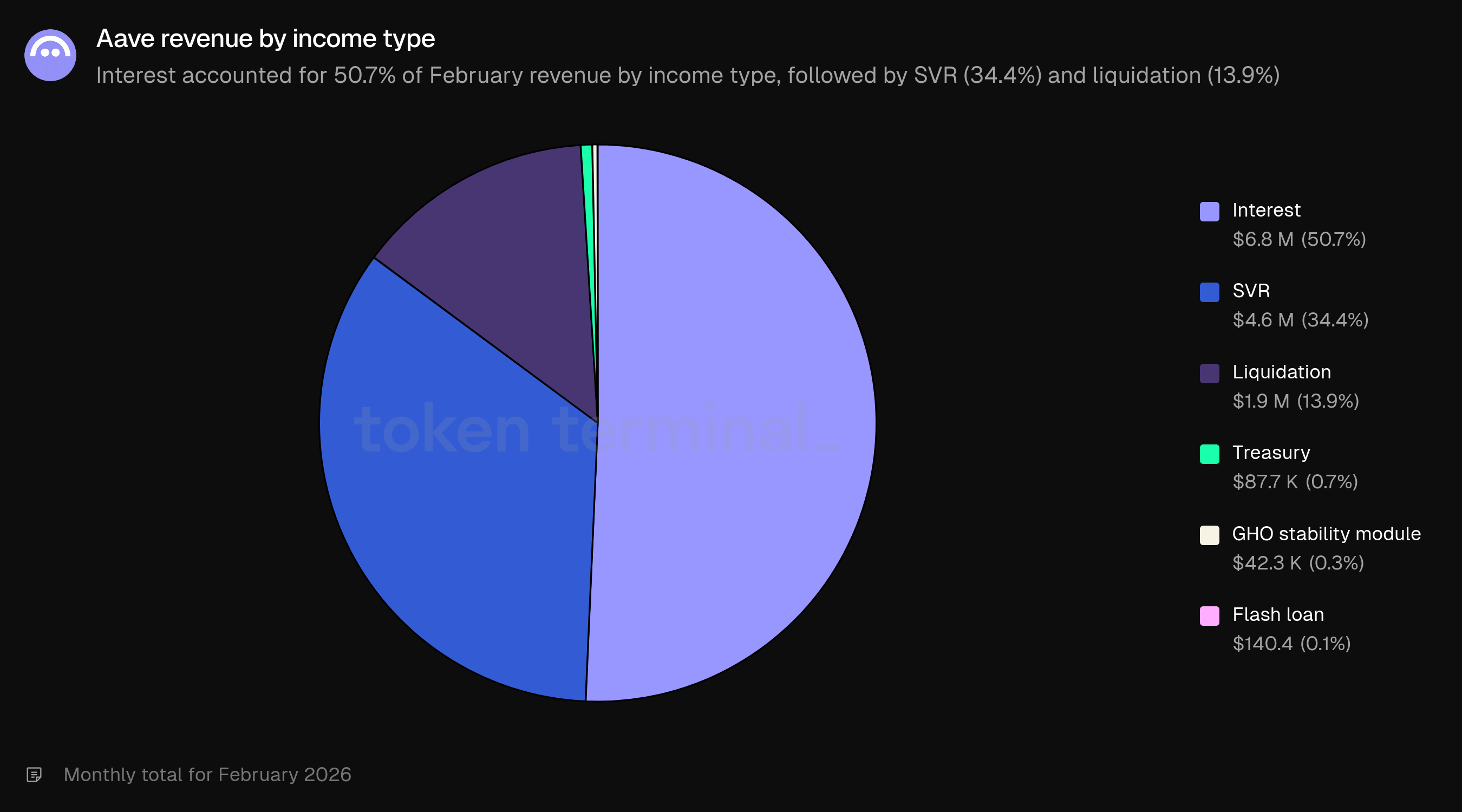

Aave's February report breaks revenue down by income type: interest at 50.7% ($6.8m), Chainlink SVR at 34.4% ($4.6m), and liquidation at 13.9% ($1.9m). Revenue here measures fees retained by the Aave DAO, not total fees paid by users. The remaining 1.0% came from treasury income, the GHO stability module, and flash loans.

The report tracks each revenue line separately, including SVR, a revenue source that doesn't show up without granular income breakdowns. When a borrower's position hits its liquidation threshold, liquidators compete to repay the debt. Chainlink SVR auctions off the right to execute these liquidations, splitting the revenue between Aave and Chainlink. Market volatility means more liquidations, which means more SVR revenue.

Token Terminal integrated SVR as a standalone income type as the line item grew in size. Now, Aave's monthly report breaks out SVR revenue separately. This makes it easy for investors to understand where the month-over-month revenue growth came from.

Where the business lives

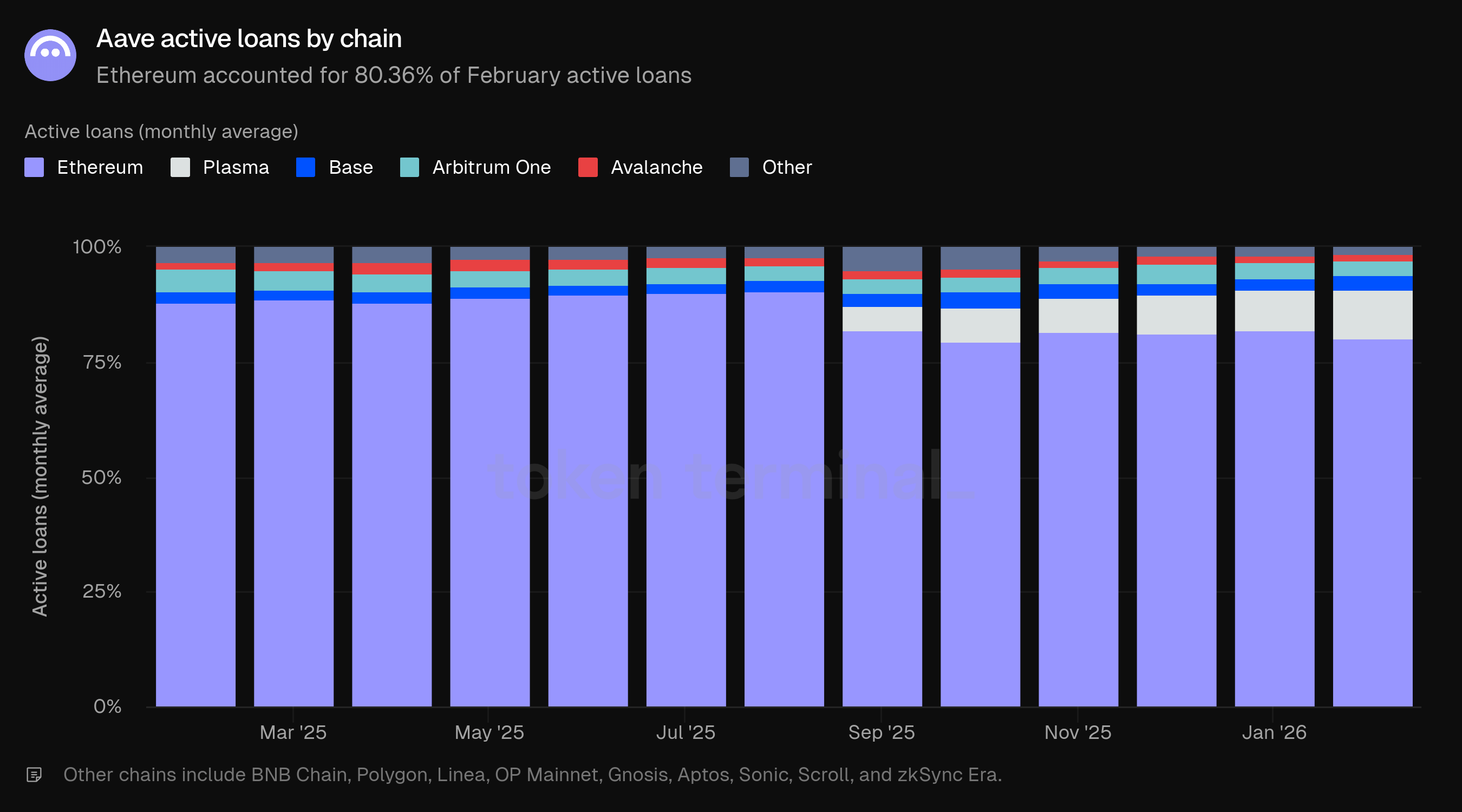

Aave's report breaks down borrowing activity by chain, showing 80.36% of February active loans concentrated on Ethereum. Plasma followed at 10.28%, Base at 3.00%, and Arbitrum One at 2.96%. Borrowing activity is heavily concentrated on mainnet.

The chain-level data shows where Aave has real borrowing demand versus where it is just deployed. The other chains are growing but account for a smaller share of actual borrowing demand. Aave is deployed across more than a dozen chains, and the distribution of loans tells investors where the project has real traction.

As Aave continues to expand to new chains, Token Terminal maintains coverage to ensure that the metrics stay accurate and comparable over time. The ability to analyze Aave's metrics by chain is important for investors that want to understand how successfully the DAO expands its business across different distribution platforms.

How Aave stacks up

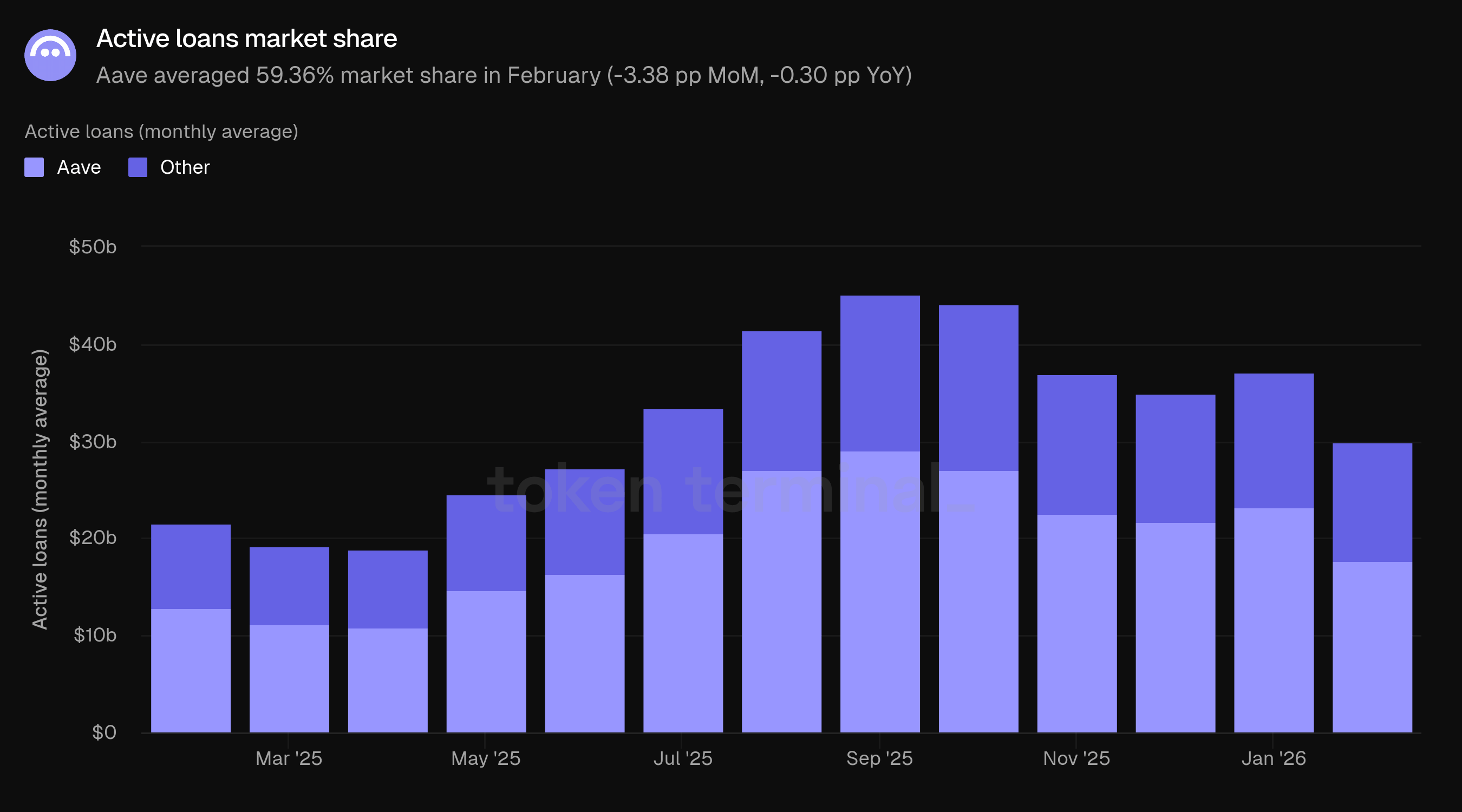

The report benchmarks Aave's active loans against the rest of the lending market sector, showing 59.36% market share in February: $17.79b out of $29.98b. Aave's active loans exceed the combined total of all its competitors.

The February data shows that Aave's dominance held through the market downturn. The long-term trend of majority market share indicates that Aave has managed to build liquidity network effects for its lending business line. The upcoming quarters will show if the DAO is able to execute at a similar level with its GHO stablecoin.

Token Terminal maintains a standardized dataset that covers the entire lending market sector. This dataset gives investors and analysts the necessary context to evaluate the performance of different lending platforms against each other in a fair and accurate manner.

Access all charts and underlying datasets here.

Aave is one example. Token Terminal has published 13 Q4 2025 reports covering Aethir, dYdX, Ether.fi, Euler, Fluid, Houdini Swap, Moonwell, Morpho, Pendle, Raydium, Silo, Solv Protocol, and TRON across lending, liquid staking, derivatives, exchanges, infrastructure, and more. Each report covers key financial and operational metrics alongside qualitative commentary from the respective core team.

In their own words:

"Significant progress was made in Q4, adding core elements like an Android app, free physical cards, and multiple types of fiat transfers."

"Fluid launched on Plasma, grew across almost every metric, and secured more partnerships and integrations in Q4."

"MAU growth on Morpho has been rapid, driven by integrations with large-scale distribution applications such as Coinbase, World App, Bitget, and more."

"Boros recorded over $6b notional volume within five months of launch, though it still represents only ~0.1% of total crypto OI."

"Raydium's balance sheet remains healthy with substantial holdings in SOL and USDC relative to costs. This is reflected by Q4 profit margins of 91%, despite the decline in overall revenue."

Access all reports on Discover

If you're evaluating how to formalize your project's data and reporting strategy, get in touch.

Platform updates:

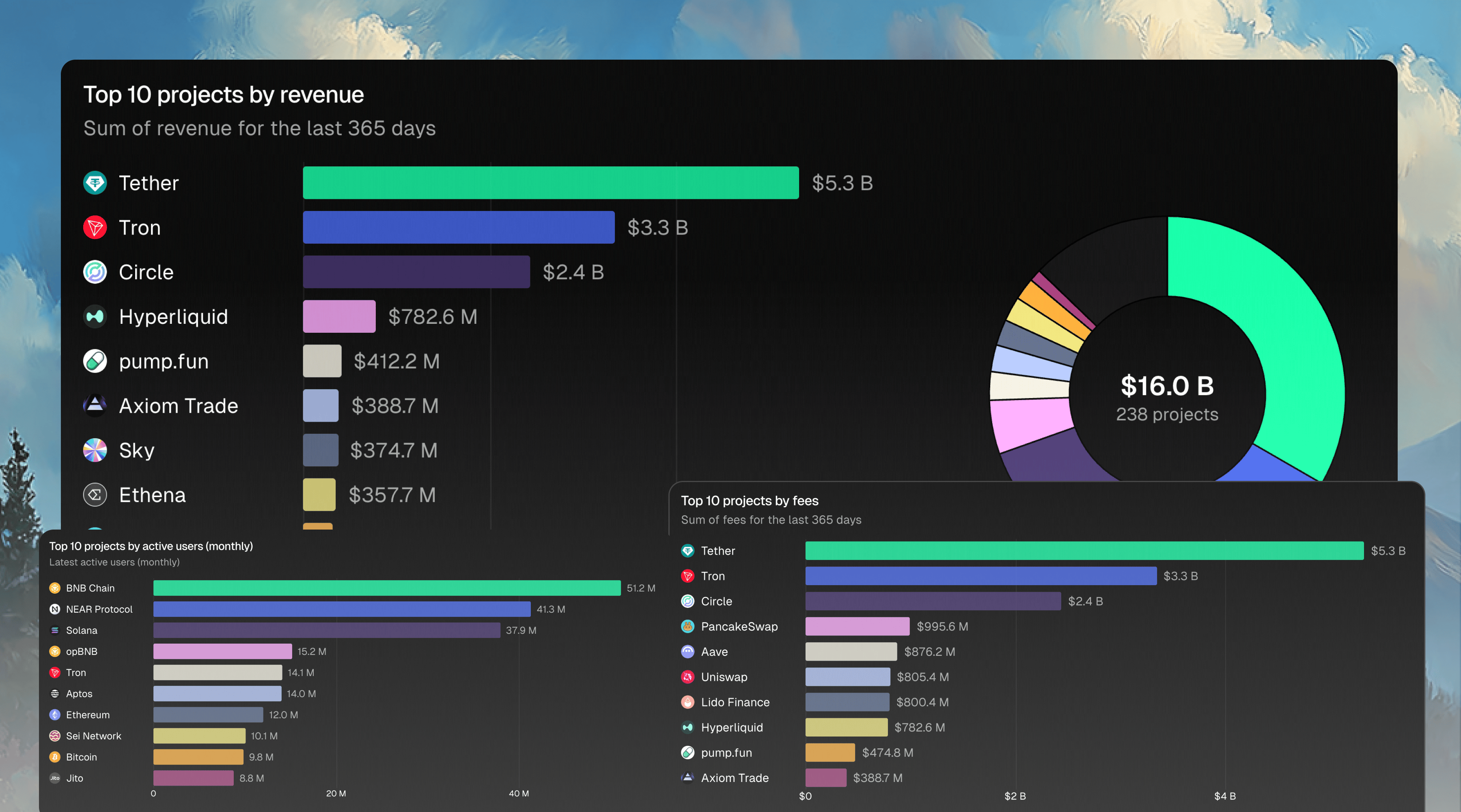

Redesigned Metrics pages. Open any metric and instantly see the top projects ranked with a horizontal bar and pie charts showing their share of the total market.

Integrated Chainlink SVR as a product of Aave. SVR recaptures value from liquidation auctions and distributes Aave's share as native ETH weekly. This revenue was previously folded into Aave V3's totals and now appears as its own line item.

Added excluded addresses to Tokenized asset methodology pages. For any asset where preminted or treasury addresses are excluded from circulating market cap calculations, the methodology now lists which addresses are excluded. For example, AAPLX (Apple xStock) by xStocks now shows 10 excluded addresses across 9 chains.

Listed DSCN (Denario Silver Coin by Tokengate), a tokenized silver commodity, on the Tokenized assets page. Total coverage now stands at 3,159 assets.

Listed 11 projects with basic metrics, including Tokengate, Humble DeFi, Alpha Arcade, GARD Protocol, and AlgoRai Finance.

Interested in getting listed? Read more here.

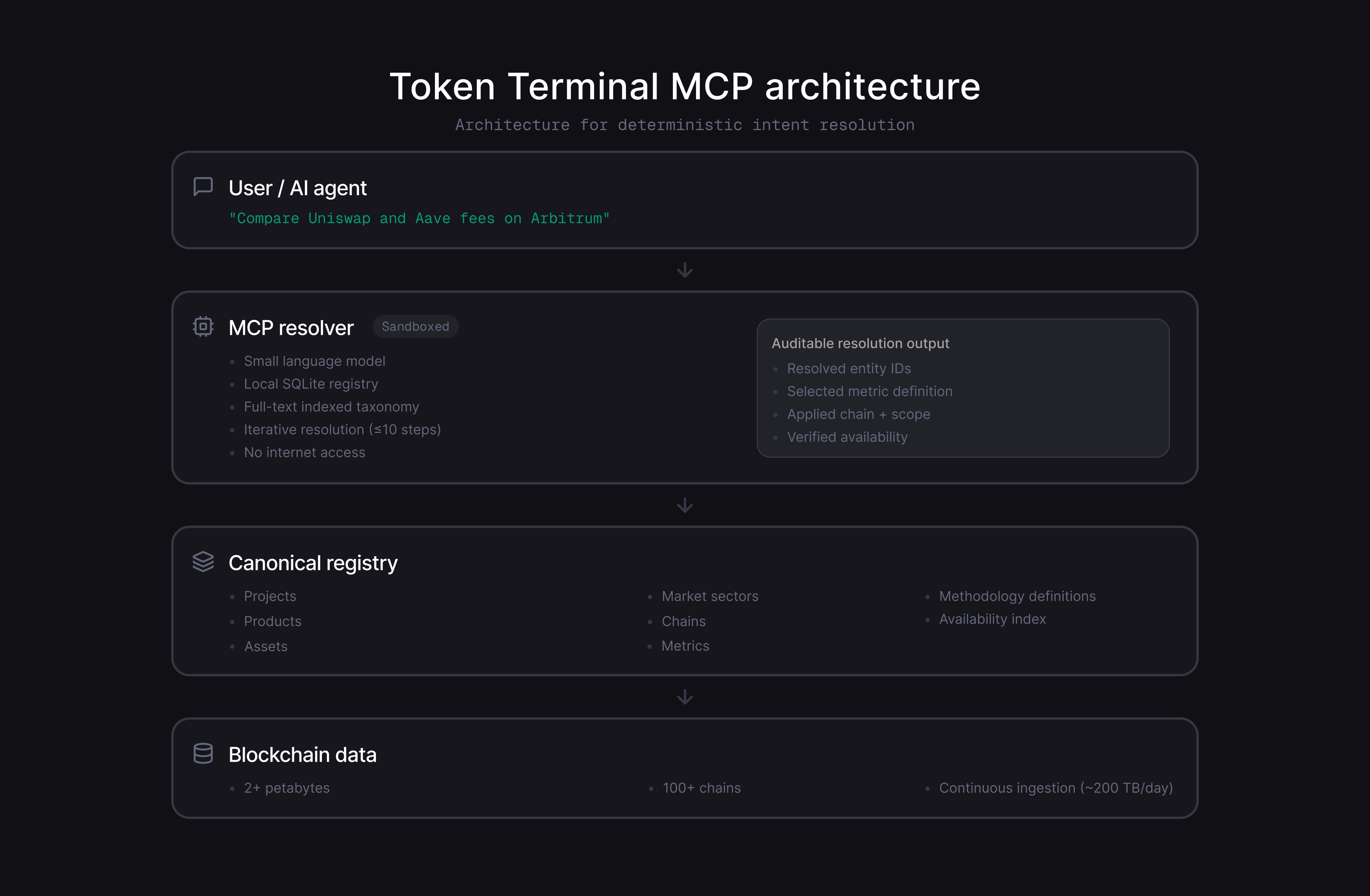

The brain behind Token Terminal's MCP server

When an AI agent asks for "Ethereum fees," the question is ambiguous: Ethereum as a network, Ethereum as an ecosystem, or a specific metric definition that varies by scope? Multiply this ambiguity across 100+ chains, 300+ projects, and 200+ metrics, and basic enumeration breaks down.

Token Terminal’s new MCP architecture replaces eight tools with one. A sandboxed language model resolves natural language queries against Token Terminal's full entity taxonomy, verifies that the requested data exists, and returns a structured response in ~200 tokens at 1 to 7 cents per call.

The result: any AI agent can query Token Terminal's data warehouse with a plain question, without needing to understand the internal taxonomy.

Interested in accessing Token Terminal's MCP? Book a demo with our team to see it in action and get a free trial.