- Token Terminal

- Posts

- The growth of tokenized real-world assets (RWAs) on Morpho

The growth of tokenized real-world assets (RWAs) on Morpho

A data-driven overview of Morpho's fastest growing business line by Token Terminal Research

1) Overview of RWA-backed lending on Morpho

Unlike loans backed by crypto-native assets such as ETH or BTC, RWA-backed lending allows borrowers to access stablecoin liquidity on Morpho using tokenized real-world assets as collateral.

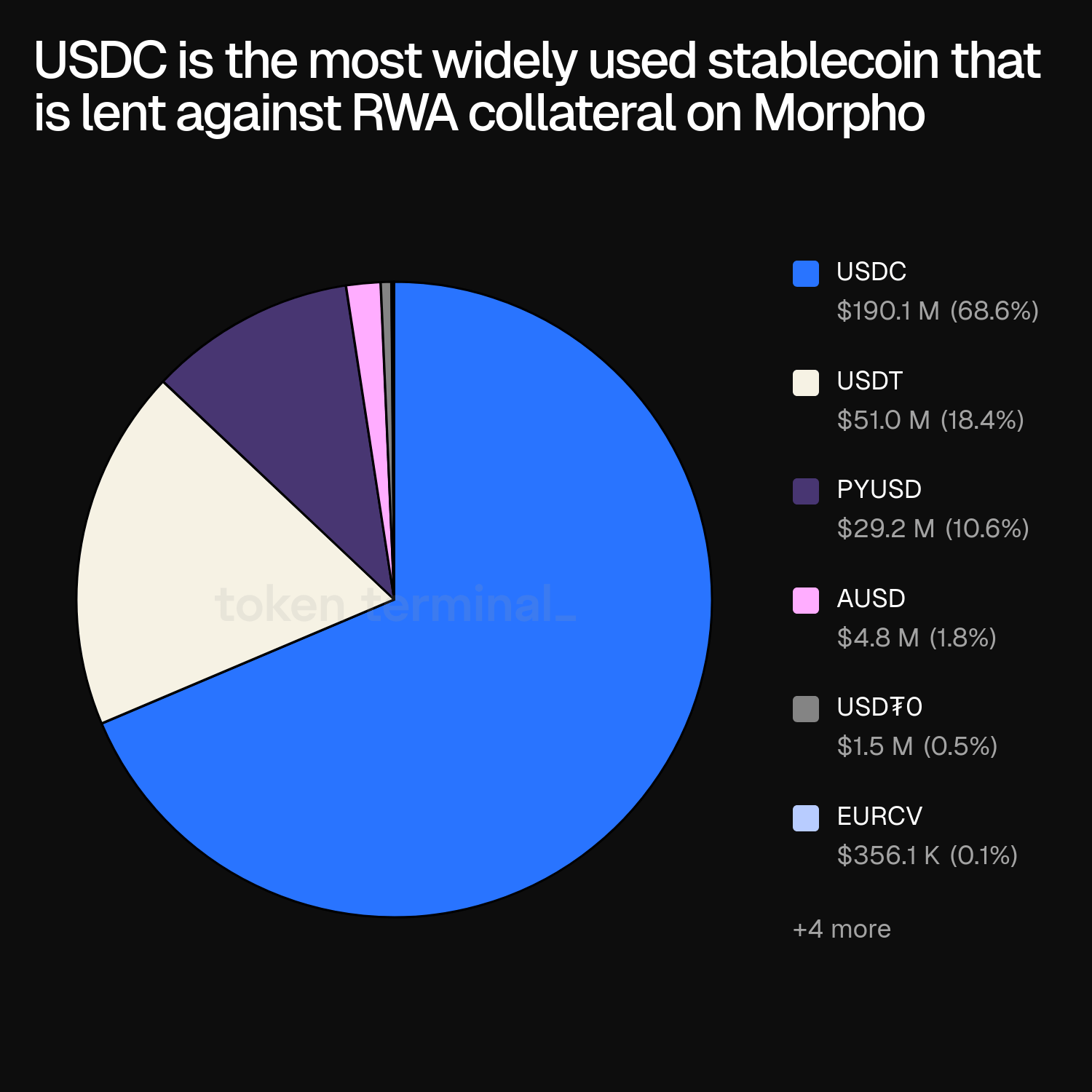

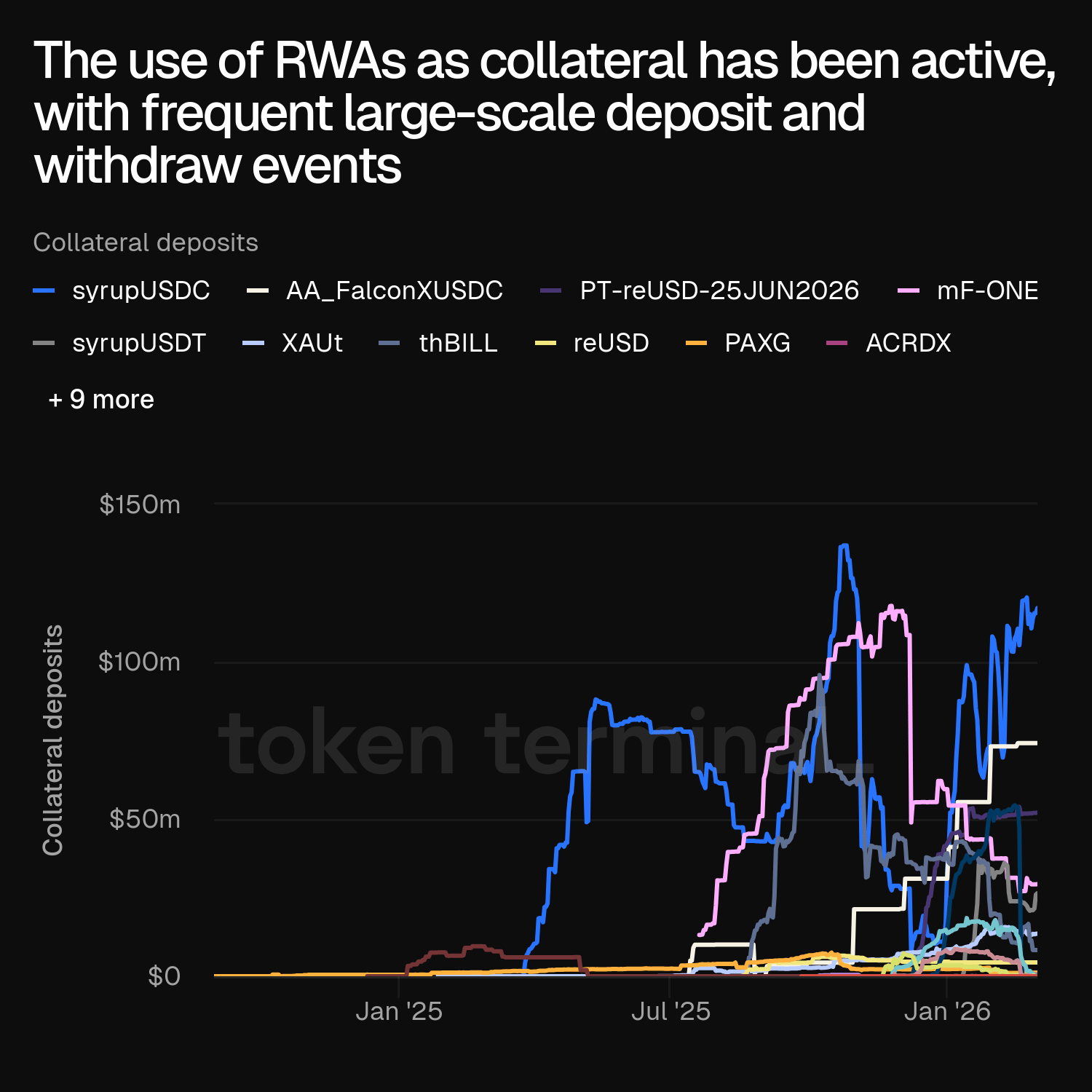

The most widely used RWA collateral assets are currently syrupUSDC, AA-FalconXUSDC, mF-ONE, thBILL, syrupUSDT, and more. These assets comprise categories like private credit, treasuries, commodities, and insurance. The most widely used loan assets are USDC, USDT, and PYUSD.

RWA collateral deposits.

Assets lent against RWA collateral.

2) Value propositions by stakeholder (lender, curator, borrower, RWA issuer, and Morpho)

From the borrower’s perspective, the key value proposition is leveraged looping (buy an RWA that yields 10% and use it as collateral to borrow stablecoins at 5%, buy more of the RWA, and repeat the loop to capitalize on the spread) and/or access to liquidity.

For lenders and curators, the emergence of RWA-collateralized markets opens up the possibility to create new strategies that target better risk-adjusted yields than strategies that only lend against crypto-native collateral assets.

From Morpho’s perspective, the key value proposition of RWA collateral is that it unlocks new scale and stability. In contrast to crypto-native collateral that’s valued at a few trillion dollars, RWA collateral markets comprise asset classes with an aggregate market cap of $400 trillion and beyond. It's a category that a leading onchain lending protocol cannot afford to miss.

Finally, the RWA issuers themselves benefit from their assets getting increased utility through a platform like Morpho; an investment exposure asset like QQQon becomes productive when used as collateral to borrow against. The improved feature set makes the tokenized asset more desirable for investors and borrowers, thereby increasing the AUM for the RWA issuer.

RWA-collateralized borrow rate.

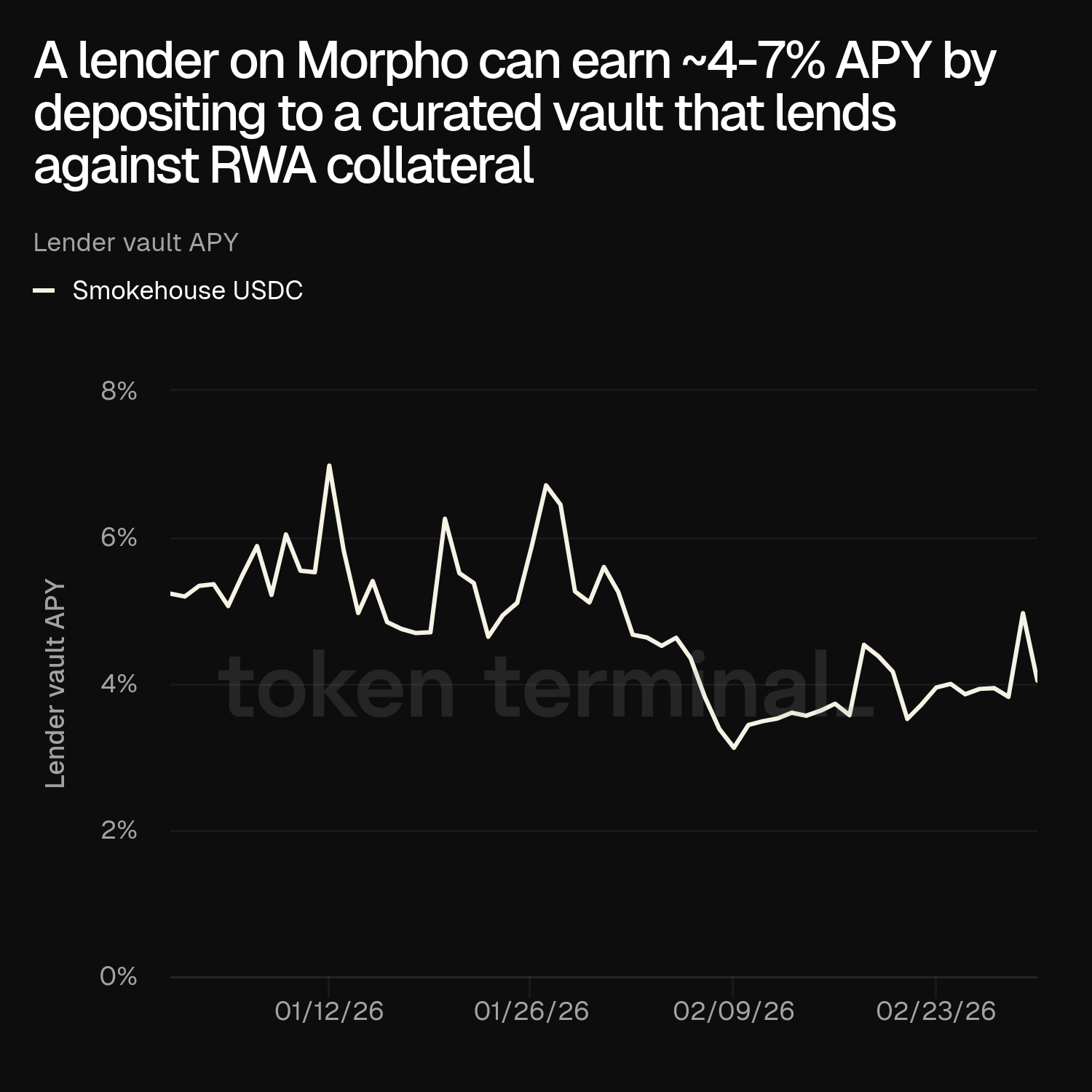

Yield when lending against RWA collateral.

3) RWAs have momentum on Morpho

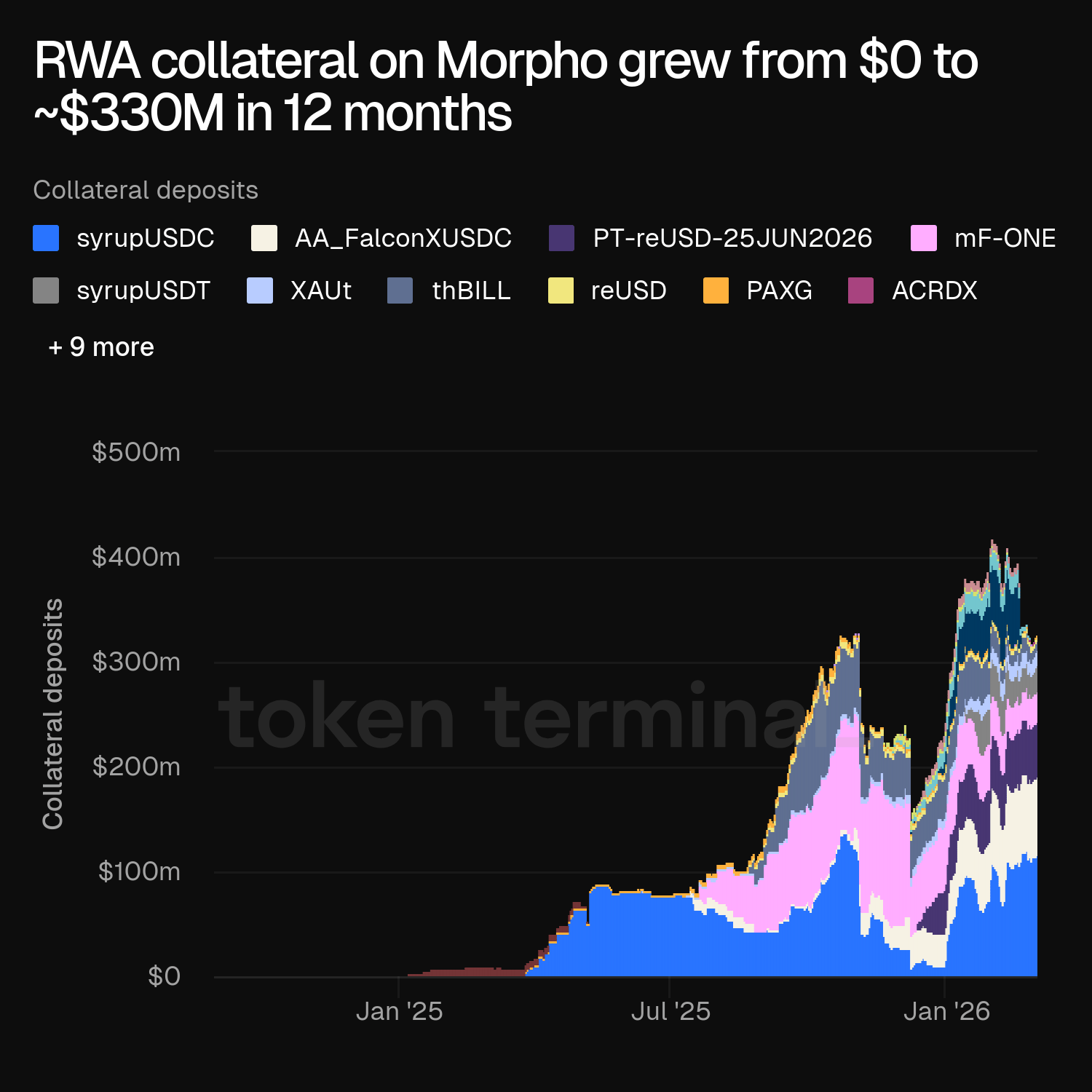

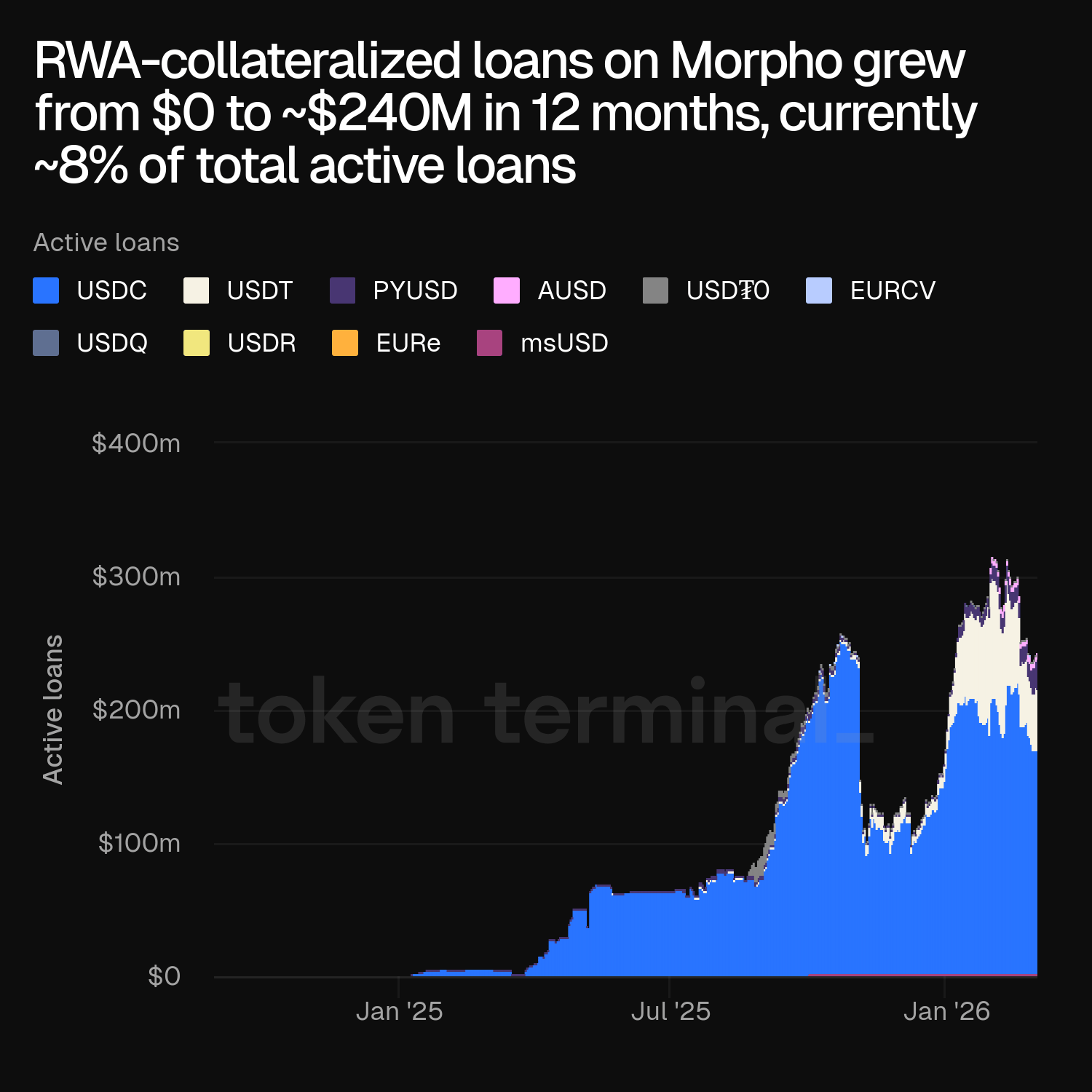

The RWA-backed lending market on Morpho grew from zero to ~$330M in collateral and ~$240M in active loans over the past year, representing ~8% of all active loans on the platform. RWA lending is currently distributed across 45 markets.

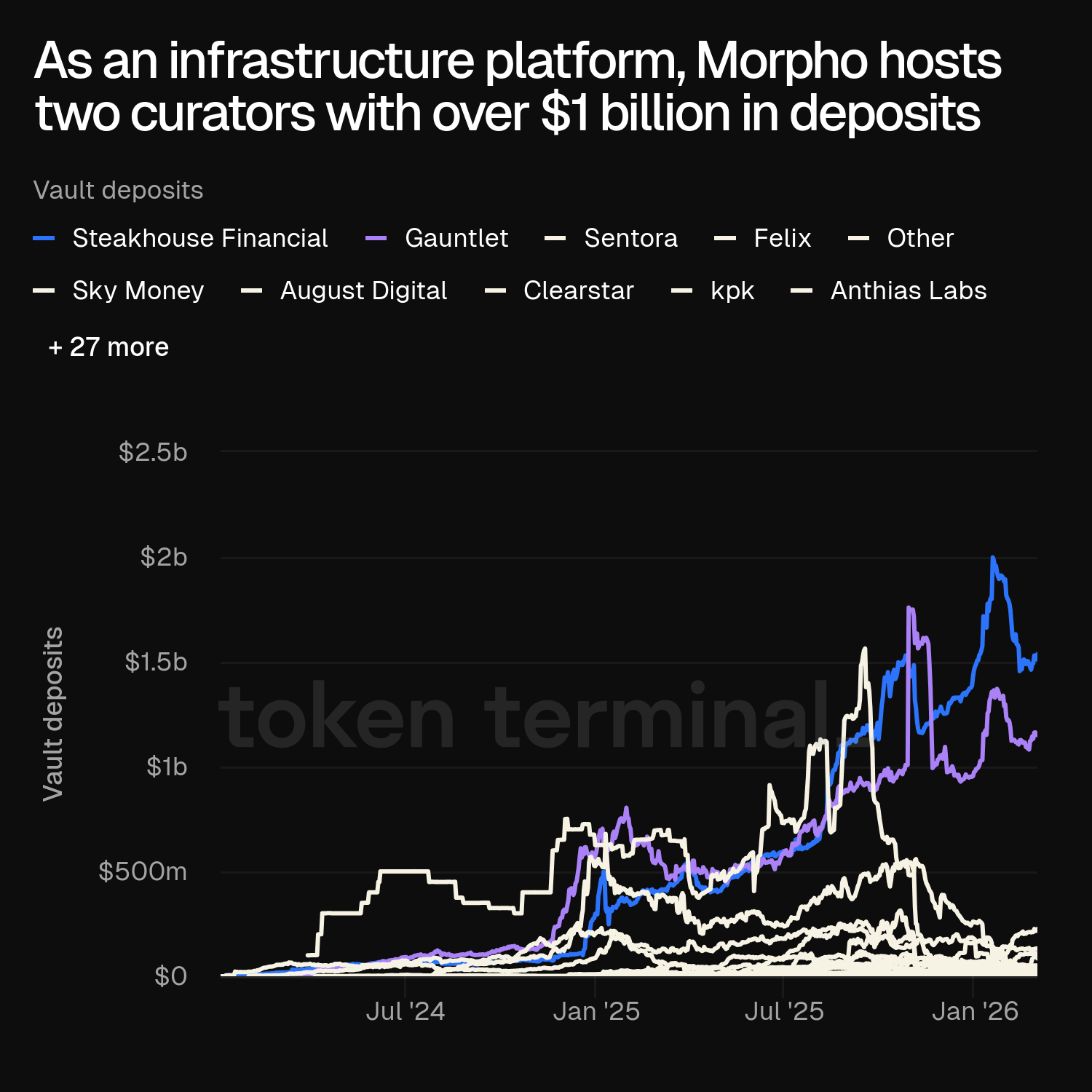

These markets are incorporated into the investment strategies of curators, like Steakhouse Financial and Gauntlet, who manage vaults or non-custodial investment funds that take in stablecoin deposits from lenders and allocate them across markets according to their vaults' pre-defined strategies.

RWA collateral deposits over time.

Active loans, collateralized by RWAs, over time.

4) Morpho's curator model is purpose-built for RWAs

RWAs introduce increased complexity. Curators that lend against RWA collateral need to perform both onchain and offchain due diligence in order to understand all the risks that relate to the tokenized RWA collateral asset and its underlying product and issuer.

Especially for RWA collateral, tracking historical onchain liquidity and volatility is not sufficient. Curators are often directly invested in the underlying offchain fund or product, which gives them access to the information required for proper risk management and safeguarding of lenders’ deposits.

This work is performed against a performance fee that’s usually between 5-10% of the yield generated by the curator’s vault.

Vault curators by total deposits.

Depositor count in RWA-focused vaults.

5) RWAs do not come without tradeoffs

The biggest risk that’s introduced by RWA collateral is the asset & liability mismatch, which is a result of lenders being accustomed to instant deposits and withdrawals, while the RWA collateral assets might enforce lengthy redemption windows.

The whole concept of over-collateralized lending relies on liquidators, who act on behalf of lenders, having the proper economic incentives to liquidate collateral before its value goes below the value of the outstanding borrows. If an RWA collateral asset doesn’t have a liquid secondary market, like e.g. ETH has onchain via DEXs, or the issuer doesn’t allow for swift redemptions at scale, a liquidator might be hesitant to get involved in the liquidation process, ultimately leaving the lender with bad debt.

RWA collateral deposits by asset.

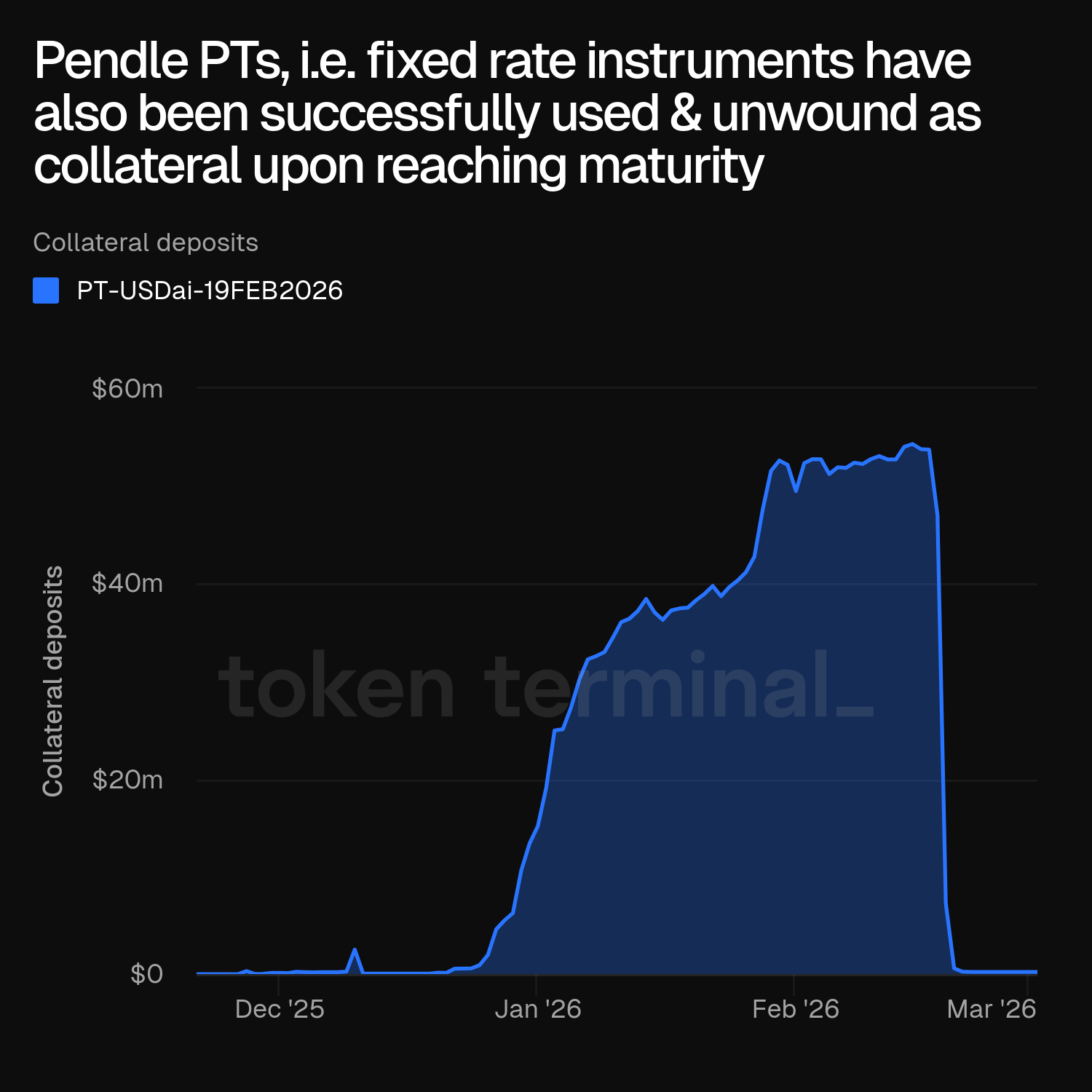

RWA collateral deposit (Pendle PT).

6) RWAs can still work great as DeFi collateral

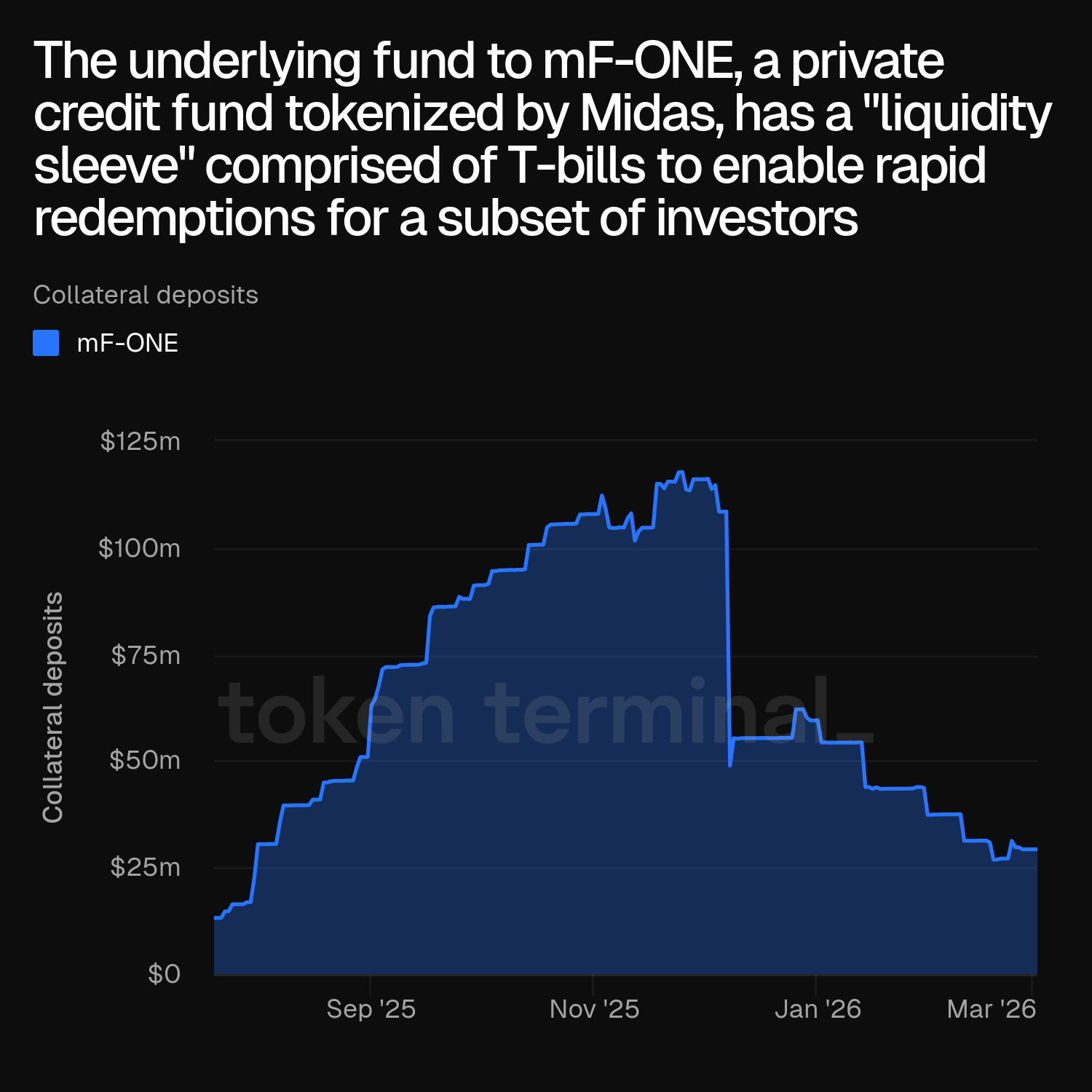

The asset & liability mismatch has been addressed in multiple different ways, e.g. through dedicated liquidity sleeves, where a small portion of the underlying fund is invested into e.g. T-Bills to accommodate for fast redemptions. This gives investors and liquidators a better user experience (liquidity), with the tradeoff of slightly lower or diluted returns.

The leading RWA issuers on Morpho, such as Maple, Pareto, Midas, Theo Network, and Pendle, are all working towards improving the user experience of RWAs as DeFi collateral.

RWA collateral deposit (mF-ONE).

Asset holders (mF-ONE).

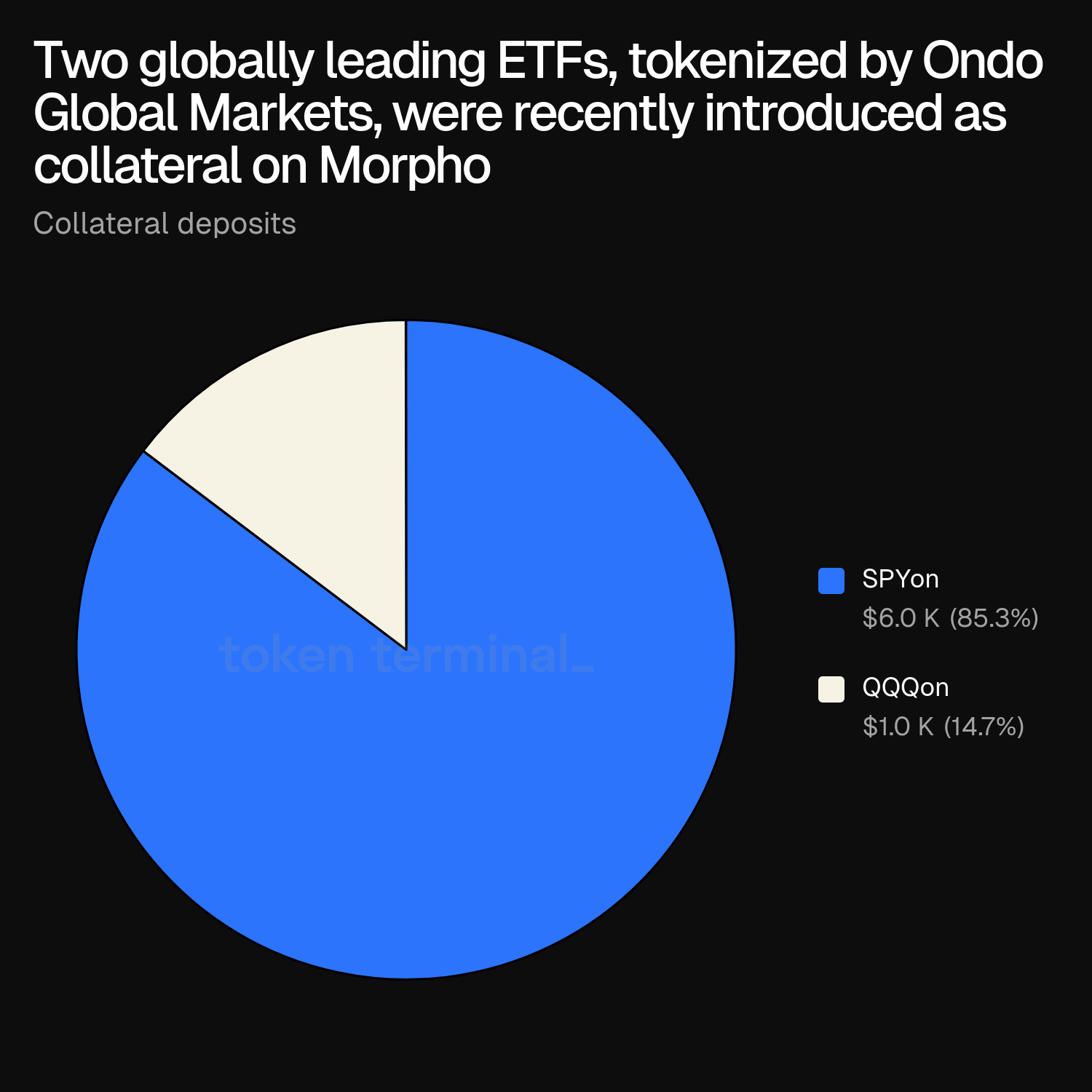

7) Future outlook for RWAs on Morpho

Morpho recently announced the integration of Ondo Global Markets’ tokenized versions of SPY and QQQ as collateral, which means that two globally leading ETFs can now be productively used in DeFi, in addition to the investment exposure that these assets give to their holders.

After this, Morpho supports each of the four main RWA markets: stablecoins (via Circle, Tether, etc.), tokenized funds (via Securitize, Midas, etc.), commodities (via Tether, Paxos, etc.), and stocks (via Ondo Finance). The RWA category, excluding stablecoins, is currently at a ~$23B market cap, growing ~300% YoY. Morpho continues to position itself to benefit from the continued growth of RWAs across different sectors.

RWA sectors by market cap.

Leading ETFs enabled as collateral.

Future work

The datasets and commentary in this dashboard will be updated on an ongoing basis.

Explore the full dashboard here.